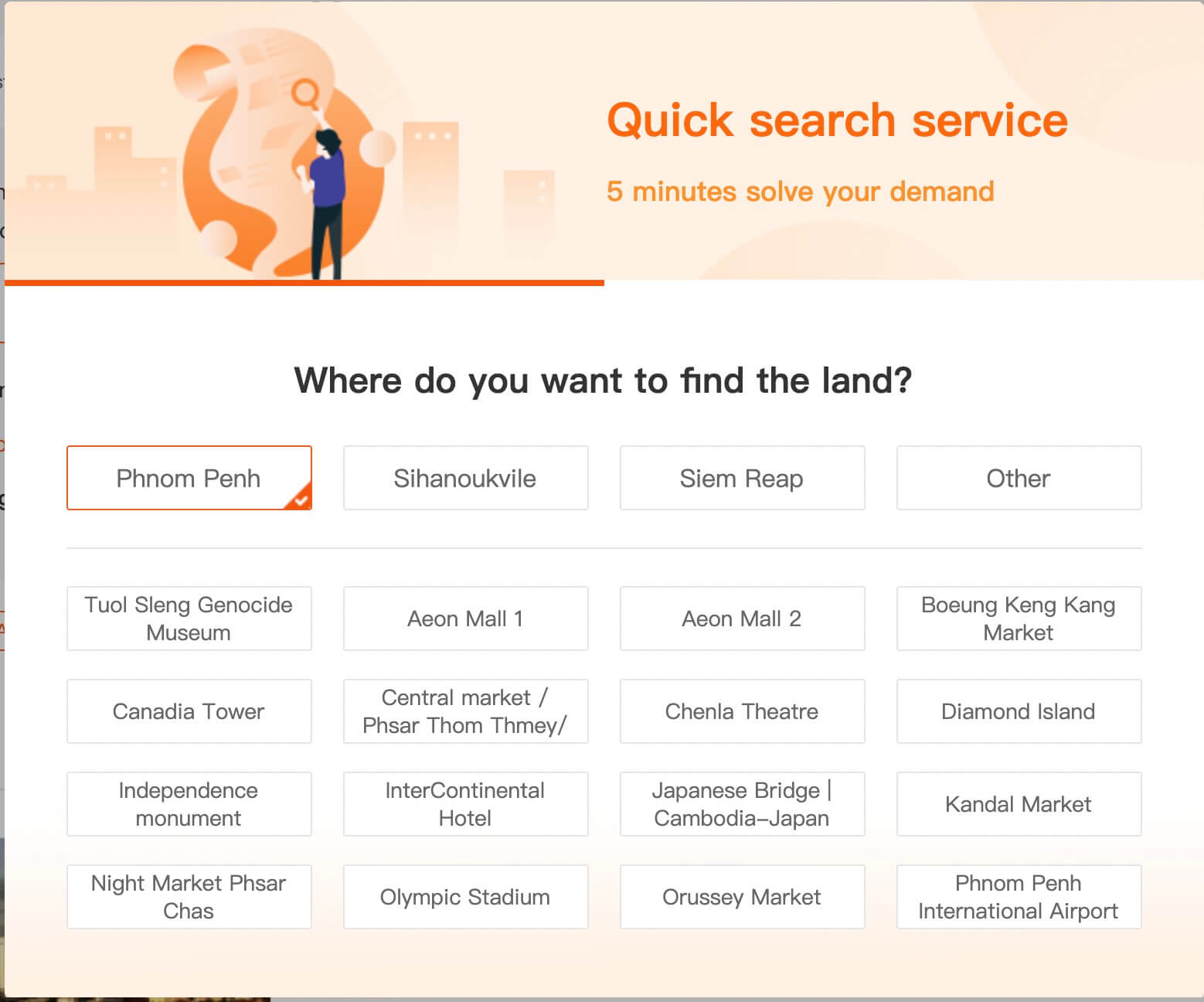

Property purchase policy

1. Non-Thai nationals cannot purchase Thai land, that is, foreigners cannot purchase permanent property buildings with land, especially villas.

2. Foreigners can buy an apartment and it is a freehold property right. The only restriction is that 51% of the property rights of the entire apartment building are hold by Thai citizens, and foreigners can purchase up to 49% of the apartment.

3. Foreigners can also buy villas or land in Thailand and have freehold property rights, but through the registration of a Thai company.

4. Foreigners can buy a home loan in Thailand. The down payment is calculated based on housing prices or valuation, which is generally 30%. But the interest rate is higher, around 5%.

5. If you want to buy an forward delivery housing by mortgage, you must pay a deposit (25% -30%) after you visit the housing, which is equivalent to a down payment. And when the housing are delivery,then you can apply for a loan.

6. Because there is no "property tax" in Thailand, you only need to pay several transfer taxes when you transfer property in Thailand.

Tax

Transfer tax | 2% of the total price, 1% for both buyer and seller |

VAT | 3.3%, within 5 years of handing in the housing and obtaining the property certificate. 0.50%, hold the property for more than 5 years or settle in for more than 7 years |

Stamp duty | 0.5%. After delivery |

Personal Income Tax |

Depending on the specific situation of the property and the holder, generally foreigners are not exempt from tax. |

Inheritance tax | Inheritance tax free |

Property management fee | 40-60 Baht / ㎡ (including all public facilities such as swimming pool and gym) |

Maintenance fund | Generally 500-600 baht / ㎡ (depending on the developer), which is a one-time fee |

Registration fees for transfer of property rights | Forward delivery housing can be transferred independently before the contract is signed and delivered, and the name change fee is required to be paid to the opener, generally 20,000-50,000 baht Existing houses or obtained real estate certificates, from the date of holding real estate certificates: Less than 5 years of sale: 7% transfer fee + 3.3% VAT; More than 5 years of sale: 7% transfer fee + 0.5% VAT |

Process of purchasing housing

1. Sign a reservation contract, pay a deposit. After selecting the unit, sign a reservation contract to order a room to determine the specific house number, sales price and payment time, and pay the booking fee according to the contract. Ordinary apartments are usually about 50,000 to 100,000 baht (about CNY 10k-20k yuan).

2. After 3-5 working days Housing purchase contract will be hand over to buyers, learn more about the content of the housing purchase contract, if there is no objection to the contract terms, sign the housing purchase contract in duplicate, after signing, buyers can keep one original and send another copy version back ( or send by Mail).

3. Pay the down payment, usually 10% -50% of the total housing price, usually need to remit the money to a personal Thai account within 2 weeks. During the construction of the property, it is necessary to pay regular interim payments on a regular basis.

4. Housing acceptance and payment of the final payment. Once the project is completed, the developer will notify the buyer of the final payment time three months before the project is delivery. Then wait for the housing to go through the mortgage or pay the full payment and receive the property ownership certificate.

5. Transfers: Buyers bring passports, bank remittance certificates and cheque to the Land Department for transfer. Generally, buyers can entrust a developer or agent to handle it for you. The formalities for property transfer in Thailand can be completed within 1 day generally.

Foreigners who are non-Thai residents and foreigners must wire the money from overseas. This means that all payments must be made to Thailand in the form of foreign exchange. The receiving bank will issue a foreign exchange transaction certificate, which will be submitted to the National Land Department when the ownership of the registered apartment is carried out.

If you do not have a bank account in Thailand, you can directly transfer the remittance to the developer's account. In this case, the developer, as the payee, will obtain a certificate of "foreign exchange transaction" from the bank on behalf of the buyer. The developer will retain all supporting documents and / or credit notes until the transfer date of the apartment unit ownership.

To obtain a foreign exchange transaction certificate, you need to:

1. The name of the remitter and buyer should be the same as possible (if someone else remits the money, please write the name of the purchased item, the buyer's name and the unit number in the remittance postscript), please fill in the full name and address of the remitter and payee.

2. Payment currency must be remitted in the form of foreign exchange. It is recommended that the major foreign currencies in US dollars, should not be remitted directly by Thai currency. They cannot be converted into Thai currency before the remit money.

3. Please specify the name of the project, buyer's name and unit number in the postscript of the remittance(cannot be wrong)

4. When paying each time, please include the handling fees of overseas and receiving banks (generally recommended to remit 50-100 USD)

Debit advice

After each payment is remitted, please send a scanned copy of the remittance slip to the developer for checking.

Payment difference

For each payment (US dollars or other currencies), it will be automatically converted to Thai currency after arriving at the local bank in Thailand, which may cause excess or insufficient amounts. Therefore, it is recommended that customers remit more (generally recommended to remit 50-100 US dollars) , The extra amount will be settled in the later payment of the purchase unit, don't worry about the waste of extra money. If the customer pays a small amount of foreign exchange, there may be a need to make up (remittance).

It is recommended to set up a non-resident bank account with a local bank in Thailand after purchasing a Thai property, so that the bank can issue a cashier's check in the future, so that you don't have to worry about problems with the company account of the remittance developer when you pay the balance of the housing.

Loan mortgage

Bank of China and Industrial and Commercial Bank of China branches in Thailand can provide loan services, and some other financial companies also provide loan services.

Transfer of property rightsThai real estate investors and real estate developers sign a purchase contract (purchased off-plan) when the property is not built or under construction. After the real estate project is completed, the full law takes effect as a legally recognized apartment unit, and the buyer and seller will register property rights in the land office Transfer procedures to obtain a re-issued contract (property certificate) with the buyer's name (the previous property certificate and property rights belong to the developer).

The buyer can request to transfer the real estate certificate account name to his own name or other legal person (property transfer). In order to prepare for the transfer and verify the legal validity of the behavior, the buyer needs to inform the seller (developer) of the property transfer behavior 60 days ago.The buyer is responsible for preparing the necessary property transfer documents. If the property certificate account is a foreigner, the buyer needs to prepare the Thai Bank ’s overseas foreign exchange remittance documents (Thailand foreign currency exchange transfer form) in the name of the buyer. That is necessary documents stipulated by Thailand law.

ROI

ROI (Return on Investment or Rental Yield), also refers to the rental income, which refers to the ratio of the rent obtained to the rent to the price of the house. The rent can be used to measure the investment income of the property and the real market demand. Rental income is important because they can help repay loans, which is the main purpose of buying investment housing.

The advantage of rent is that the investment risk is low and it can generate cash flow, which helps protect investors from interest rate shocks while reducing the potential demand for continuous cash input.Of course, when real estate is sold, capital appreciation is likely to be lower than that of houses with strong capital growth (detached houses), especially considering the impact of the compound annual appreciation rate of the housing, which is its most obvious disadvantage.

Capital Gain

Capital Gain or Capital Growth, that is, the value of the property ’s existing assets minus the price at the time of purchase, the value earned or lost. That is, when the held variable sale assets (such as stocks or real estate) are sold, the selling price is higher than the original purchase cost, that is, a profit is generated, and this profit is the realized capital gain.When considering the purchase of capital-value-added houses, it is the goal of every investor to obtain considerable capital growth. In the long run, the strong annual growth rate of capital should be defined as the inflation rate plus 3%-5%, so the capital appreciation rate should be maintained between 5 and 7%.

Disclaimer: The re-forward articles on Compass website are for the purpose of conveying more information, and it does not mean that the Compass website agrees with its views or confirms the authenticity of its content. Article noted as "Source: Compass original", please note that the source from Compass. The content of the article is for reference only and should not consider as investment advice, and it does not mean that Compass agree with its views.

0

+855 (0) 23222206 (CN/EN/KH)

+86 023 67480241 (CN)

+855 (0) 66400666 (CN/EN/KH)

cpassre@gmail.com

cpassre@gmail.com

https://www.compass.com.kh

https://www.compass.com.kh

Office Building Ground floor, Kbal Dey No. 594, Street Wat Chas, Phum 01, Sangkat Chroy Changva, Khan Chroy Changva, Phnom Penh

Office Building Ground floor, Kbal Dey No. 594, Street Wat Chas, Phum 01, Sangkat Chroy Changva, Khan Chroy Changva, Phnom Penh